Innovative and creative services/solutions developed by utilising new technologies in every sector proved us, that it is possible to manage a lucrative business while providing efficient and delightful customer journey. Therefore customer expectations are getting higher — always pursuing agile and personalised solutions; and financial services customers are no different. So what does this mean for the future of the financial world, still dominated mostly by the traditional institutions with their bureaucracy, legacy systems and cumbersome cultures, and how does this all affect the customer experience?

Traditional Financial Institutions: Can’t Keep up with Customer Expectations

Needless to say, the financial industry is the core of a functioning economy, serving to 4 main functions:

- Credit Provision: Channelling the flow of funds from savers and borrowers, financial institutions allow businesses to invest and households to spend more than their actual savings. In that sense, banks play a crucial role in boosting economic growth.

- Liquidity Provision: In case of a temporary cash flow problem, businesses and households turn to financial institutions to access liquidity. Financial institutions help them either to cover their debts quickly by withdrawing their deposits or borrowing in the form of loans.

- Provision of Payments Services: Financial institutions affect and facilitate the processing of payments, which is the indispensable part of both trade and economic life.

- The Creation of Markets: Taking part in money market transactions and lending to one another and to companies, financial institutions are indispensable players in making markets to raise capital and transfer liquidity and risk.

Until a couple of years, traditional financial institutions were meeting customer needs more or less- or customers weren’t so acquainted that they could get a better service. And even though traditional financial institutions were not meeting the customer expectations, they were still considered as the secure and trustable foundations, able to scale and overcome regulatory compliances- well, until the 2008 financial crisis.

After that, the concerns about what the finance industry could do to the global economy arose, and it turned out there can always be a risk in the current system. With the addition of customers realising that they are not receiving the financial services they need in regards to personalisation, agility and flexibility or traditional financial services being too costly (e.g for SMEs); it was time for the financial industry to be reshaped.

The Rise of FinTechs

Since it became so clear that it was no longer enough for the financial industry to continue offering what has worked for them in the past, the gaps caused by traditional financial institutions emerged FinTech firms.

What do FinTechs bring to the table?

In every sector, technology is reshaping how the companies do business, the way they offer services, and it enables organisations to target niche areas easier. In the finance industry; FinTech firms are now providing customer-centric services in almost every segment (banking- BankTech, insurance-InsurTech, wealth management -WealthTech, payments- PayTech), and create new business models for selling financial products/services. Let’s see in which areas FinTechs are changing the landscape of the finance industry by utilising Big Data, Artificial Intelligence (AI), Blockchain, Cloud and Mobility.

Peer-to-peer (P2P) lending: FinTechs have introduced the industry to a new business model where the technology brings savers and borrowers directly together (removing the middleman) which will significantly transform the lending business and SME financing. Various lending platforms offer services from students to high-potential borrowers and investors.

Customer-centric products and solutions: Fintech firms now align with customer goals with agility and an improved customer journey. They are able to analyse the journey from the customer’s perspective and able to redesign in a more efficient way. With the effective use of customer data through big data analytics Fintechs provide;

- Higher personalization: It is now possible to offer customers personalised advice/services/products based on customers’ risk analysis, behaviours, preferences and even lifestyle and social affiliations/ preferences. For instance, InsurTech companies gain deeper customer insights by using other technologies such as wearables (life insurance, health insurance), and telematics (vehicle insurance) in order to offer personalised services. For example telematics (in-vehicle telecommunication devices) enable insurers to identify whether the drivers are likely to be involved in an accident, or have their car stolen, by combining various data. IoT devices and wearables (Fitbit, Apple Watch etc.) allow InsurTech firms to track their customers in order to predict and calculate risks.

- Increased speed and efficiency of services: By the help of real-time updates and mobile connectivity etc, FinTechs can provide faster services. For example Stripe, a payment platform, enabled merchants to launch a website and start accepting payments within minutes (when up to 7 days were needed to set up a new merchant)

- Seamless omnichannel engagement across all customer touchpoints: call centre, mobile, branch, internet etc

- Quick response & 24/7 availability

- Better functionality & simplifying the customer experience

- Simpler interfaces: Design-based thinking across the customer lifecycle eliminates multiple pain points

- More affordable services: With not having the cost of the legacy infrastructure, and by the help of robotic process automation technology (robo-advisors, chatbots) FinTech firms can offer lower-priced services.

Utilising advanced big data analytics: Taking advantage of big data analytics enable Fintech firms to better risk management, underwriting capability, and allow them to offer their customers tailored solutions. For example using predictive analysis & modeling firms can offer their customers personalised solutions based on their behaviour as well as prompting customers for fraud prevention or money-saving opportunities.

Penetrating niche segments: With advanced distributions and innovative low-cost solutions (AI based automations, robo-advisors etc.) FinTech firms are able to offer affordable services to niche segments traditional financial institutions have never reached.

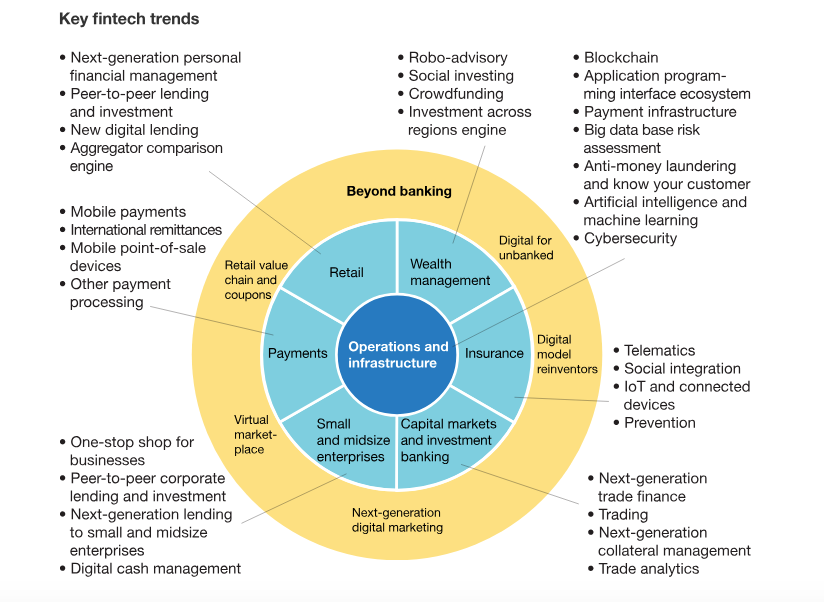

Below you will see a diagram created by McKinsey showing us there are more than 30 areas emerging as new norms, and this is just in banking;

Conclusion

FinTechs have been targeting the finance industry focusing on innovative and superior products/ services and already started to fill the gaps left by traditional financial institutions throughout the customer journey. However, there are still some areas beyond FinTechs’ capabilities and this love-hate relationship between FinTechs and traditional institutions is starting to turn into collaboration. We will see more BigTechs constituted by both parties, leveraging each others core strengths, and competencies.

Read more at Commencis Thoughts

![]()

How FinTechs are disrupting the finance industry was originally published in Commencis on Medium, where people are continuing the conversation by highlighting and responding to this story.